Interest Rates, set by central banks (or in our case the Federal Reserve), are essentially the rates at which banks charge one another for very short-term (overnight) loans. It is also the rate at which the central banks charge commercial banks for holding their reserves (i.e., JP Morgan, Bank of America, Citi, etc.). When the economy isn’t doing too hot, central banks tend to lower Interest Rates to encourage consumer spending and business investment (borrowing), which they hope will in turn stimulate economic growth.

↓ interest rate => ↓ interest rate for loans => ↑ incentive for consumers and businesses to spend

Since the recession in 2008, central banks around the world have tried to reinvigorate their respective economies by engaging in two primary activities: quantitative easing (QE) and near zero interest rate policy (ZIRP). The big problem is, is that neither of these have worked. The U.S. is actually worse off now compared to 2008, Europe is in deep shit (even more so now with the Syrian migrant crisis), Japan is creeping closer and closer to hyperinflation (QE since 1990s..oops), and the BRIC countries are all struggling to find new avenues for growth.

QE is a policy where central banks increase their economy’s money supply by buying assets from governments/banks in order to provide them with additional liquidity and to promote lending.

QE (a.k.a “free money”) has made the rich richer by providing financial institutions with a “hall pass” on all the shitty loans they weren’t supposed to make and allowed them to shore up their balance sheets (so they could make more loans). While the near ZIRP (a.k.a “cheap money”) started a malicious cycle of malinvestment by both consumers and businesses, which have created massive bubbles across various asset classes (public/private equities, real estate, oil/energy loans, auto loans, etc). It’s comical that, even though the primary cause of our previous banking crisis was the over consumption of debt, central banks have engaged in policies to encourage more of it.

While these expansionary monetary policies have acted as a steroid for temporary economic relief (at least on the surface), our central banks have only treated the symptoms of the disease, not the cause. Trying to solve a debt problem by creating more it, has only further exacerbated our original problem. And this is exactly why the next economic crisis will be more painful compared to 2008. Whether the correction happens this year or 10 years from now, the longer the policy makers continue to “kick the can,” the more severe the next recession will be.

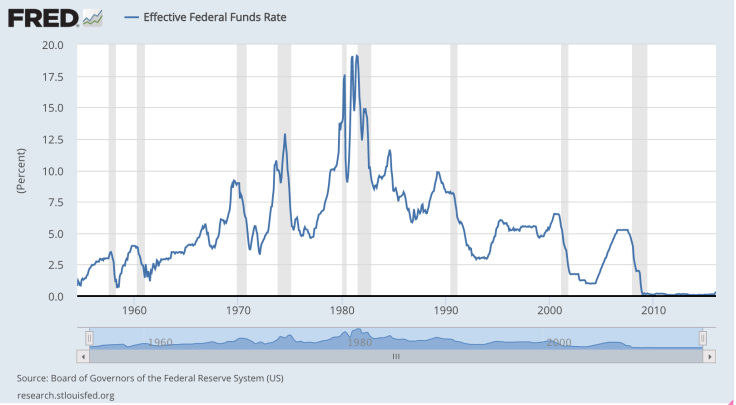

The Federal Reserve has made “one” right decision by ending QE (at least for now), but the ongoing near ZIRP is still doing more harm than good in the long-term. The longer the rates are kept artificially low, the greater amount of capital will be misallocated and the bigger the bubbles will become. As shown below, the Federal Reserve has already kept Interest Rates near 0% for the last 6+ years:

Since the ZIRP (alongside QE for some time as well) has failed to spur the desired economic growth and inflation, the Federal Reserve is now considering pouring more gas into an already flaming economy by turning to Negative Interest Rate Policy (NIRP). As of today, five central banks (European Central Bank, Switzerland, Sweden, Dutch and Bank of Japan) have already implemented NIRP. To understand how upside down our society would be with NIRP, let’s take a quick look at the two examples below:

The Saver:

- Put $100 in savings account

- Annual Interest Rate: -5% (for simplicity’s sake, I know this is exaggerated)

- Savings account shrinks to $95 by end of the year

The Borrower:

- Borrow $100 from Bank

- Annual Interest Rate: -5%

- Bank actually pays Borrower $5, which is used to pay down existing principal

- Borrower’s principal amount shrinks to $95 by end of year

Saving is already tough enough for the 76%+ of the U.S. population who live paycheck to paycheck (this figure is probably higher now), and now policy makers want to make it even more difficult to save for a reasonable vacation, car, house, or better yet, retirement (something the government definitely won’t be helping with)? And on the flip side, if banks are essentially paying people to take out loans, how many people will try to “qualify” for loans their personal incomes don’t justify?

To be fair, commercial banks currently feeling the wrath of NIRP have not yet passed on their negative interest rates (added cost) to their consumers – so as of now us Savers are still safe. But if banks continue to lay people off and suffer from declining profits, at some point, they will need to pass on their added cost to the consumer, which could lead to massive runs on banks (where everyone and their mom withdraws cash from their accounts) and put the economy in even deeper shit.

This is also another reason why you should never vote for a “cashless” society…

For now, Borrowers hoping to get paid for taking out loans is also an unlikely scenario as long as the negative interest rates stay low enough. Remember, the interest rates set by central banks are for short-term (overnight) loans. Therefore if commercial banks create loans for longer time horizons (6 month, 1 month, 1 year, etc.), they will receive a higher interest rate (time premium) and still profit from the transaction. No central bank should be idiotic enough to drive interest rates negative enough for a borrower to be able to call himself an investor, but that remains to be seen.

As Albert Einstein once said, “the definition of insanity is doing the same thing over and over again, but expecting different results.” The Federal Reserve has kept Interest Rates near 0% for over half a decade and it hasn’t worked. Maybe it’s time to finally try something new and instead engage in policy that will restrict the amount of “cheap money” floating around in our economy.

Yes, if interest rates are raised to where they should be, our economy will suffer and wealth will be destroyed. There will be a massive wave of loan defaults by both corporations and individuals. The stock market will implode. Many tech companies won’t be able to live up to their valuations. Our own Federal Government will have a tougher time making interest payments on its growing amount of debt. Export-based companies nationwide will suffer as our currency continues to appreciate. And much more.

But lessons will be learned. People will become more knowledgable on personal finance (hopefully), the businesses left standing will be more sound financially and the misallocated capital before will now either be destroyed or flow naturally back to the appropriate asset classes. Since we live in a world with central banks (I don’t believe they should exist) where they are constantly interfering with the free market, with every boom, there is a guaranteed bust. And like when you’re in a shitty relationship, it’s always better to go bust, sooner rather than later.

Leave a comment